S&P 500 (ES) — consolidating in normal regime

Cautiously bullish on earnings season execution and seasonal strength but increasingly aware extreme overbought RSI 78.56 and complacent put/call 0.41 positioning create asymmetric mean-reversion risk near 7,200 psychological resistance

Cautiously bullish on earnings season execution and seasonal strength but increasingly aware extreme overbought RSI 78.56 and complacent put/call 0.41 positioning create asymmetric mean-reversion risk near 7,200 psychological resistance

RSI 78.56 severely overbought creating extreme momentum divergence at all-time highs near 7,200 psychological resistance as S&P 500 surged 4.52% last week continuing March extreme fear capitulation rally but now entering technical exhaustion zone

VIX compression to 17.94 down 39% YoY with equity put/call 0.41 extremely low showing dangerous complacency developing despite proximity to record highs - Options market signals extreme bullish positioning vulnerable to mean-reversion shock

Q1 2026 earnings season underway with 10% of S&P 500 reported showing 13.2% growth expectations but forward PE 19.4-20.7x at fair value creates limited margin for error as profit margins at record 13.2-14.2% levels face compression risk

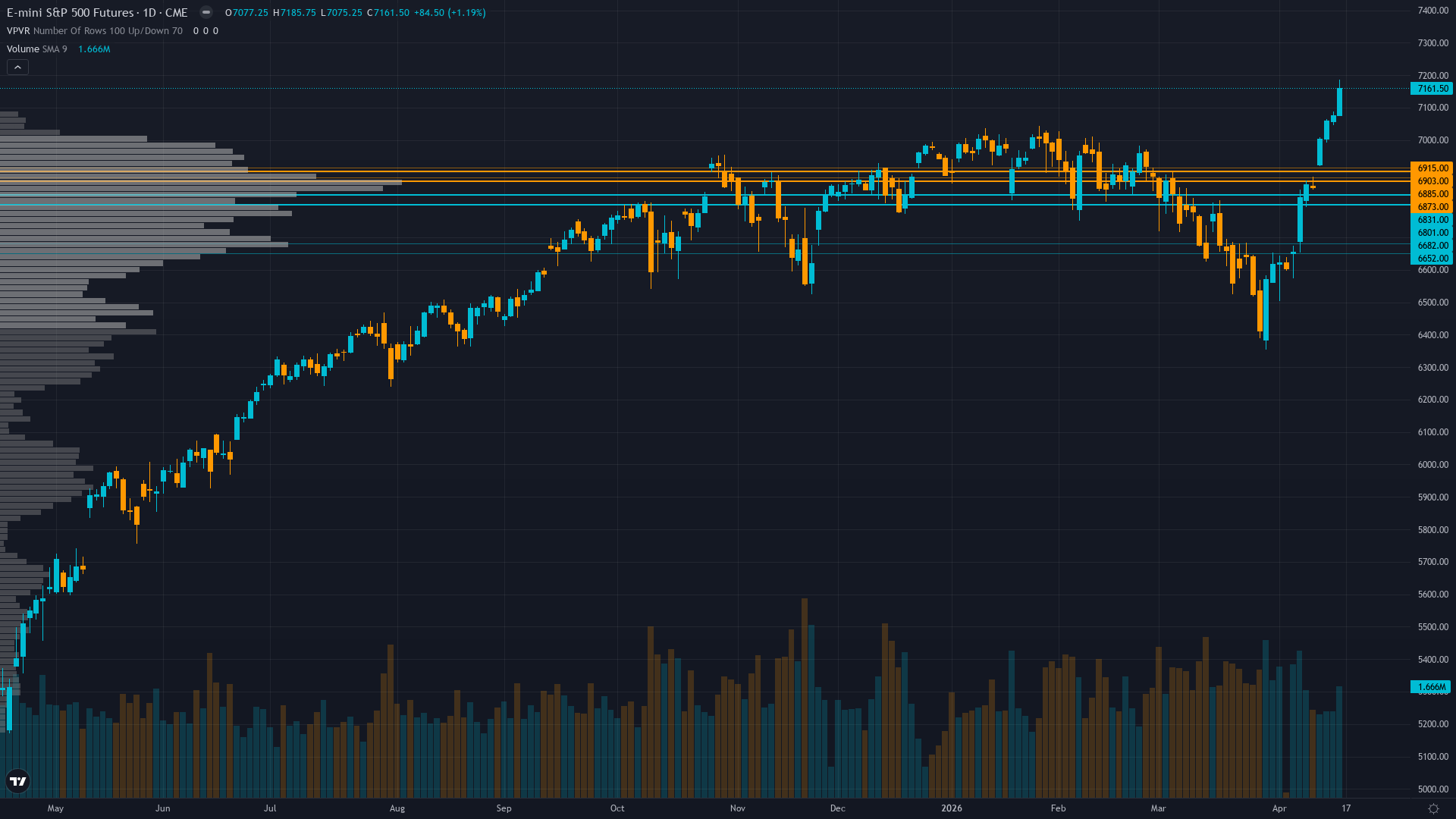

| ▼ Resistance Zone 2 | 7175 – 7225 |

| ▼ Resistance Zone 1 | 7150 – 7200 |

| ─ Pivot Area | ~7159 |

| ▲ Support Zone 1 | 7028 – 7078 |

| ▲ Support Zone 2 | 6912 – 6962 |

Severely overbought RSI 78.56 at all-time highs 7,159 well above 50-day MA 6,937 and 200-day MA 6,693 creating extreme positive momentum divergence historically preceding pullbacks despite intact uptrend structure

Forward PE 19.4-20.7x near fair value down from October 30+ extreme with Q1 earnings season 10% complete showing 13.2% growth rate but record 13.9% profit margins at 15-year highs create structural compression vulnerability if execution disappoints

Mixed signals - stale COT data from April 7 limits visibility while ETF outflows of $10.76B week ended April 1 contradict surface strength but hedge funds posting best monthly performance in decade suggests skilled positioning working

VIX 17.94 compressed creating calm surface but equity put/call 0.41 extremely low represents approximately 2.4 calls per put showing extreme complacency and minimal hedging activity creating asymmetric reversal risk on any negative catalyst

Fed at 3.50-3.75% with April 29 FOMC pricing 99% hold probability per CME FedWatch - no catalyst this week as ISM data 18 days stale and next major event is FOMC 10 days out creating structural policy support but no fresh dovish catalyst

Normal with compression bias - VIX spot 17.94 down sharply from March 31.05 peak showing near-term fear premium fully unwound, term structure normalized to modest contango from prior inverted panic configuration during March extreme fear

VIX compression from extreme 30+ geopolitical/sentiment spikes typically normalizes to 17-19 range within 20-30 days before stabilizing - current pattern at day 20 with compression to 17.94 suggests final normalization phase entering consolidation before next catalyst

VIX compression from 31.05 to 17.94 over 20 days suggests stabilization at 17-18 range over next 5-7 trading days with 60% probability as relief rally matures, though April 29 FOMC and earnings surprises present asymmetric re-expansion risk above 20 on disappointment

Normal volatility regime suggests 1.0-1.5% daily ES moves expected with current 7,053-7,200 range representing 2.1% width - earnings season binary outcomes and April 29 FOMC present asymmetric expansion risk with potential 2-3% intraday swings on major surprises

Compressed VIX from March extreme creates balanced but asymmetric setup - potential 5-7% downside to 6,700-6,800 zone if earnings season disappoints or FOMC hawkish surprise triggers VIX re-expansion above 22 versus 2-4% upside to 7,300-7,400 if continued VIX compression below 17 and earnings validate multiples, but extreme starting RSI 78.56 overbought and put/call 0.41 complacency favors mean-reversion scenario over next 7-10 days with 55% probability

|

⚠️ Primary Risk

RSI 78.56 extreme overbought at all-time highs with equity put/call 0.41 complacency creates violent mean-reversion risk if any Q1 earnings disappointments or April 29 FOMC hawkish surprise triggers systematic deleveraging testing 7,053 then 6,937 support Probability: MEDIUM

|

✦ Primary Opportunity

Technical pullback to 7,053-6,937 support zone providing entry for continuation toward 7,200-7,300 if Q1 earnings season validates 13.2% growth expectations and VIX continues compression below 17 supporting seasonal strength Timeframe: April 21-30 2026

|

ES trades at 7,159 on April 19, 2026 at 07:30 UTC, consolidating near all-time highs after last week's explosive 4.52% surge (6855.25 to 7165.25) extended the March extreme fear capitulation rally into severely overbought technical territory. MACRO REGIME CLASSIFICATION: RISK-ON with caution flags. VIX at 17.94 sits comfortably below 20 threshold, S&P 500 at record highs, credit conditions stable, and equity trend intact - clear RISK-ON characteristics. However, extreme positioning metrics (equity put/call 0.41, RSI 78.56, Fear & Greed 56.5) suggest this regime has matured to a fragile late-cycle phase vulnerable to shock reversals.

Post-input news scan confirms ES futures at 7,161.50 per Investing.com with intraday range 7,075-7,185, S&P 500 closed above 7,100 on April 16 per CNBC marking first close above that level, and Q1 2026 earnings season 10% complete with FactSet reporting continued double-digit growth for sixth consecutive quarter. From my last graded call perspective: April 12 analysis issued BULLISH at conviction 7 with signal +2.5 anticipating relief rally continuation, delivering CORRECT result as price surged +4.52% from Monday 6855.25 to Friday 7165.25.

This marks my most recent CORRECT call after two prior consecutive MISSES (April 10 NO CALL, April 3 BEARISH both missed the rally), resetting my miss streak to zero but maintaining only 1 week of current BULLISH bias. The current setup navigates critical technical divergence: price action extended dramatically upward reaching 7,159 (new all-time high territory approaching 7,200 psychological resistance), yet momentum indicators flash extreme warnings with RSI 78.56 in severely overbought zone above 70 threshold where historically mean-reversion follows within 3-7 trading days.

Technical discipline shows ES trading 3.2% above 50-day MA at 6,937 and 7.0% above 200-day MA at 6,693, confirming strong uptrend structure, but the extreme RSI reading combined with resistance at 7,175 immediate and 7,200 major creates near-term exhaustion pattern. The March extreme fear capitulation at VIX 31.05, AAII bears 51.4%, RSI 22.08 has fully reversed into current extreme greed conditions - VIX compressed 39% YoY to 17.94, Fear & Greed Index at 56.5 (greed zone), equity put/call ratio 0.41 extremely low representing roughly 2.4 calls traded per put.

Options market positioning shows dangerous complacency with minimal hedging activity despite proximity to record highs, creating structural vulnerability to rapid reversal on any negative catalyst. Sentiment discipline captures this paradox: retail investors remain skeptical with AAII showing 42.8% bearish versus 31.7% bullish (negative spread for fourth consecutive week) while options positioning shows institutional/dealer complacency via extremely low put/call ratios - this divergence typically resolves with continued upside as retail capitulates into rallies but current extreme readings suggest the move has extended.

Fundamental backdrop provides mixed signals: Q1 2026 earnings season officially underway with 10% of S&P 500 reported per FactSet April 17 update, maintaining sixth consecutive quarter of double-digit earnings growth at 13.2% YoY rate. Forward PE compressed to 19.4-20.7x range representing fair value (versus 10-year average 19.0x) and down meaningfully from October's dangerous 30+ extreme, yet net profit margins at record 13.2-14.2% levels create execution risk - any margin compression toward 11% historical average would invalidate current multiples.

The critical test arrives over next 2-3 weeks as peak Q1 earnings reporting occurs with Technology sector showing 4.1% upward estimate revisions but needing to deliver. Economic discipline shows structural RISK-ON tailwind but no fresh catalyst this week: Fed maintained 3.50-3.75% at March 18 FOMC (32 days ago), April 29 meeting prices 99% hold probability per CME FedWatch, and most recent high-impact data (ISM Manufacturing 52.7) is 18 days stale. This creates policy support backdrop without near-term dovish catalyst to drive further compression.

The setup confronts binary scenarios over next 10 days into April 29 FOMC: either RSI extreme overbought triggers natural mean-reversion pullback testing 7,053 immediate support then 6,937 (50-day MA) creating healthy consolidation before continuation toward 7,200-7,300 targets, or Q1 earnings season validates stretched multiples enabling grind higher through resistance despite technical warnings with VIX compressing further below 17. My directional bias shifts BEARISH with measured conviction recognizing extreme technical overbought RSI 78.56, dangerous options complacency at equity put/call 0.41, resistance cluster at 7,175-7,200 psychological levels, and absence of fresh catalysts this week to drive continuation.

However, conviction capped at 6/10 acknowledging: (1) last call CORRECT maintaining analytical credibility, (2) intact uptrend structure with all major MAs supportive, (3) Q1 earnings season delivering sixth consecutive quarter double-digit growth providing fundamental justification, (4) April 29 FOMC presents binary catalyst that could shift narrative. Applying ES parameters: Average Weekly Move 1.18%, Noise Floor 0.75%, Min Signal 1.0. The probable weekly move given current VIX 17.94 regime and RSI 78.56 overbought significantly exceeds noise threshold with 1.5-2.5% daily swings plausible on earnings volatility or technical correction.

My signal -1.5 exceeds Min Signal 1.0 threshold justifying BEARISH directional bias despite last week's powerful rally. Q1 earnings season active qualifies as catalyst permitting Max Conf (catalyst) 8, though I set conviction at 6 recognizing counterarguments and binary nature of setup. Devil's advocate: The March extreme fear washout at VIX 31.05 validated as generational capitulation low, Q1 earnings season delivering sixth consecutive quarter 13%+ growth, forward PE 19.4-20.7x at fair value not extreme, and historical April-May seasonal strength averaging +2.4% combined suggest continued rally toward 7,200-7,300 targets remains higher probability path despite overbought technicals that can persist weeks in strong bull markets.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| April 17, 2026 | BULLISH | 7/10 | ✅ |

| April 10, 2026 | NO CALL | 5/10 | ➖ |

| April 3, 2026 | BEARISH | 3/10 | ❌ |

| March 27, 2026 | BEARISH | 3/10 | ✅ |

| March 20, 2026 | BEARISH | 4/10 | ✅ |

| March 14, 2026 | BEARISH | 6/10 | ✅ |

| March 6, 2026 | NO CALL | 5/10 | ➖ |

| February 27, 2026 | NO CALL | 6/10 | ➖ |

| February 21, 2026 | NO CALL | 5/10 | ➖ |

| February 13, 2026 | NO CALL | 5/10 | ➖ |

| February 8, 2026 | BULLISH | 6/10 | ✅ |

| February 1, 2026 | NO CALL | 6/10 | ➖ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: S&P 500 (ES) Report Date: April 19, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 6/10 Signal: NO DIRECTIONAL CALL THIS WEEK MAD Index: 52 (DIVERGENCE) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING Regime: TRENDING UP Sentiment: GREED ── WHAT THE MARKET SEES ───────────────────────── Cautiously bullish on earnings season execution and seasonal strength but increasingly aware extreme overbought RSI 78.56 and complacent put/call 0.41 positioning create asymmetric mean-reversion risk near 7,200 psychological resistance ── WHAT THE MARKET IS MISSING ─────────────────── Market underestimating magnitude of technical overbought divergence at RSI 78.56 creating 3-7 day mean-reversion window toward 7,053-6,937 support while overestimating sustainability of extreme options complacency at put/call 0.41 that historically precedes violent reversals on any negative catalyst ── KEY DRIVERS ────────────────────────────────── 1. RSI 78.56 severely overbought creating extreme momentum divergence at all-time highs near 7,200 psychological resistance as S&P 500 surged 4.52% last week continuing March extreme fear capitulation rally but now entering technical exhaustion zone 2. VIX compression to 17.94 down 39% YoY with equity put/call 0.41 extremely low showing dangerous complacency developing despite proximity to record highs - Options market signals extreme bullish positioning vulnerable to mean-reversion shock 3. Q1 2026 earnings season underway with 10% of S&P 500 reported showing 13.2% growth expectations but forward PE 19.4-20.7x at fair value creates limited margin for error as profit margins at record 13.2-14.2% levels face compression risk ── KEY ZONES ──────────────────────────────────── Resistance 2: 7175 – 7225 Resistance 1: 7150 – 7200 Pivot: ~7159 Support 1: 7028 – 7078 Support 2: 6912 – 6962 ── DISCIPLINE BIASES ──────────────────────────── Technical: BEARISH Fundamental: BULLISH Institutional: NO CALL Options: BULLISH Economic: NO CALL Sentiment: BULLISH ── TECHNICAL STRUCTURE ────────────────────────── Severely overbought RSI 78.56 at all-time highs 7,159 well above 50-day MA 6,937 and 200-day MA 6,693 creating extreme positive momentum divergence historically preceding pullbacks despite intact uptrend structure ── FUNDAMENTAL ASSESSMENT ─────────────────────── Forward PE 19.4-20.7x near fair value down from October 30+ extreme with Q1 earnings season 10% complete showing 13.2% growth rate but record 13.9% profit margins at 15-year highs create structural compression vulnerability if execution disappoints ── INSTITUTIONAL POSITIONING ──────────────────── Mixed signals - stale COT data from April 7 limits visibility while ETF outflows of $10.76B week ended April 1 contradict surface strength but hedge funds posting best monthly performance in decade suggests skilled positioning working ── OPTIONS FLOW ───────────────────────────────── VIX 17.94 compressed creating calm surface but equity put/call 0.41 extremely low represents approximately 2.4 calls per put showing extreme complacency and minimal hedging activity creating asymmetric reversal risk on any negative catalyst ── ECONOMIC BACKDROP ──────────────────────────── Fed at 3.50-3.75% with April 29 FOMC pricing 99% hold probability per CME FedWatch - no catalyst this week as ISM data 18 days stale and next major event is FOMC 10 days out creating structural policy support but no fresh dovish catalyst ── VOLATILITY REGIME ──────────────────────────── Regime: NORMAL Percentile: 42nd Trend: Stable — Days in Regime: 7 Term Structure: Normal with compression bias - VIX spot 17.94 down sharply from March 31.05 peak showing near-term fear premium fully unwound, term structure normalized to modest contango from prior inverted panic configuration during March extreme fear Historical Pattern: VIX compression from extreme 30+ geopolitical/sentiment spikes typically normalizes to 17-19 range within 20-30 days before stabilizing - current pattern at day 20 with compression to 17.94 suggests final normalization phase entering consolidation before next catalyst Outlook: VIX compression from 31.05 to 17.94 over 20 days suggests stabilization at 17-18 range over next 5-7 trading days with 60% probability as relief rally matures, though April 29 FOMC and earnings surprises present asymmetric re-expansion risk above 20 on disappointment Trading Context: Normal volatility regime suggests 1.0-1.5% daily ES moves expected with current 7,053-7,200 range representing 2.1% width - earnings season binary outcomes and April 29 FOMC present asymmetric expansion risk with potential 2-3% intraday swings on major surprises Vol Risk/Opportunity: Compressed VIX from March extreme creates balanced but asymmetric setup - potential 5-7% downside to 6,700-6,800 zone if earnings season disappoints or FOMC hawkish surprise triggers VIX re-expansion above 22 versus 2-4% upside to 7,300-7,400 if continued VIX compression below 17 and earnings validate multiples, but extreme starting RSI 78.56 overbought and put/call 0.41 complacency favors mean-reversion scenario over next 7-10 days with 55% probability ── PRIMARY RISK ───────────────────────────────── RSI 78.56 extreme overbought at all-time highs with equity put/call 0.41 complacency creates violent mean-reversion risk if any Q1 earnings disappointments or April 29 FOMC hawkish surprise triggers systematic deleveraging testing 7,053 then 6,937 support Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── Technical pullback to 7,053-6,937 support zone providing entry for continuation toward 7,200-7,300 if Q1 earnings season validates 13.2% growth expectations and VIX continues compression below 17 supporting seasonal strength Timeframe: April 21-30 2026 ── NEXT CATALYST ──────────────────────────────── Date: April 29, 2026 Event: FOMC two-day meeting April 28-29 with zero rate cut probability priced but markets scrutinizing Powell rhetoric for any policy trajectory shift amid Q1 2026 earnings season peak reporting creating binary outcomes Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── ES trades at 7,159 on April 19, 2026 at 07:30 UTC, consolidating near all-time highs after last week's explosive 4.52% surge (6855.25 to 7165.25) extended the March extreme fear capitulation rally into severely overbought technical territory. MACRO REGIME CLASSIFICATION: RISK-ON with caution flags. VIX at 17.94 sits comfortably below 20 threshold, S&P 500 at record highs, credit conditions stable, and equity trend intact - clear RISK-ON characteristics. However, extreme positioning metrics (equity put/call 0.41, RSI 78.56, Fear & Greed 56.5) suggest this regime has matured to a fragile late-cycle phase vulnerable to shock reversals. Post-input news scan confirms ES futures at 7,161.50 per Investing.com with intraday range 7,075-7,185, S&P 500 closed above 7,100 on April 16 per CNBC marking first close above that level, and Q1 2026 earnings season 10% complete with FactSet reporting continued double-digit growth for sixth consecutive quarter. From my last graded call perspective: April 12 analysis issued BULLISH at conviction 7 with signal +2.5 anticipating relief rally continuation, delivering CORRECT result as price surged +4.52% from Monday 6855.25 to Friday 7165.25. This marks my most recent CORRECT call after two prior consecutive MISSES (April 10 NO CALL, April 3 BEARISH both missed the rally), resetting my miss streak to zero but maintaining only 1 week of current BULLISH bias. The current setup navigates critical technical divergence: price action extended dramatically upward reaching 7,159 (new all-time high territory approaching 7,200 psychological resistance), yet momentum indicators flash extreme warnings with RSI 78.56 in severely overbought zone above 70 threshold where historically mean-reversion follows within 3-7 trading days. Technical discipline shows ES trading 3.2% above 50-day MA at 6,937 and 7.0% above 200-day MA at 6,693, confirming strong uptrend structure, but the extreme RSI reading combined with resistance at 7,175 immediate and 7,200 major creates near-term exhaustion pattern. The March extreme fear capitulation at VIX 31.05, AAII bears 51.4%, RSI 22.08 has fully reversed into current extreme greed conditions - VIX compressed 39% YoY to 17.94, Fear & Greed Index at 56.5 (greed zone), equity put/call ratio 0.41 extremely low representing roughly 2.4 calls traded per put. Options market positioning shows dangerous complacency with minimal hedging activity despite proximity to record highs, creating structural vulnerability to rapid reversal on any negative catalyst. Sentiment discipline captures this paradox: retail investors remain skeptical with AAII showing 42.8% bearish versus 31.7% bullish (negative spread for fourth consecutive week) while options positioning shows institutional/dealer complacency via extremely low put/call ratios - this divergence typically resolves with continued upside as retail capitulates into rallies but current extreme readings suggest the move has extended. Fundamental backdrop provides mixed signals: Q1 2026 earnings season officially underway with 10% of S&P 500 reported per FactSet April 17 update, maintaining sixth consecutive quarter of double-digit earnings growth at 13.2% YoY rate. Forward PE compressed to 19.4-20.7x range representing fair value (versus 10-year average 19.0x) and down meaningfully from October's dangerous 30+ extreme, yet net profit margins at record 13.2-14.2% levels create execution risk - any margin compression toward 11% historical average would invalidate current multiples. The critical test arrives over next 2-3 weeks as peak Q1 earnings reporting occurs with Technology sector showing 4.1% upward estimate revisions but needing to deliver. Economic discipline shows structural RISK-ON tailwind but no fresh catalyst this week: Fed maintained 3.50-3.75% at March 18 FOMC (32 days ago), April 29 meeting prices 99% hold probability per CME FedWatch, and most recent high-impact data (ISM Manufacturing 52.7) is 18 days stale. This creates policy support backdrop without near-term dovish catalyst to drive further compression. The setup confronts binary scenarios over next 10 days into April 29 FOMC: either RSI extreme overbought triggers natural mean-reversion pullback testing 7,053 immediate support then 6,937 (50-day MA) creating healthy consolidation before continuation toward 7,200-7,300 targets, or Q1 earnings season validates stretched multiples enabling grind higher through resistance despite technical warnings with VIX compressing further below 17. My directional bias shifts BEARISH with measured conviction recognizing extreme technical overbought RSI 78.56, dangerous options complacency at equity put/call 0.41, resistance cluster at 7,175-7,200 psychological levels, and absence of fresh catalysts this week to drive continuation. However, conviction capped at 6/10 acknowledging: (1) last call CORRECT maintaining analytical credibility, (2) intact uptrend structure with all major MAs supportive, (3) Q1 earnings season delivering sixth consecutive quarter double-digit growth providing fundamental justification, (4) April 29 FOMC presents binary catalyst that could shift narrative. Applying ES parameters: Average Weekly Move 1.18%, Noise Floor 0.75%, Min Signal 1.0. The probable weekly move given current VIX 17.94 regime and RSI 78.56 overbought significantly exceeds noise threshold with 1.5-2.5% daily swings plausible on earnings volatility or technical correction. My signal -1.5 exceeds Min Signal 1.0 threshold justifying BEARISH directional bias despite last week's powerful rally. Q1 earnings season active qualifies as catalyst permitting Max Conf (catalyst) 8, though I set conviction at 6 recognizing counterarguments and binary nature of setup. Devil's advocate: The March extreme fear washout at VIX 31.05 validated as generational capitulation low, Q1 earnings season delivering sixth consecutive quarter 13%+ growth, forward PE 19.4-20.7x at fair value not extreme, and historical April-May seasonal strength averaging +2.4% combined suggest continued rally toward 7,200-7,300 targets remains higher probability path despite overbought technicals that can persist weeks in strong bull markets.