EUR/USD (6E) — Desk NO CALL stance fully aligns with market noise threshold reality and…

EUR/USD consolidation in 1.15-1.18 range through March with neutral bias after dual central banks delivered expected holds removing catalyst

EUR/USD consolidation in 1.15-1.18 range through March with neutral bias after dual central banks delivered expected holds removing catalyst

Post-dual central bank consolidation with both FOMC and ECB delivering holds as expected March 18-19, removing immediate catalyst while Iran geopolitical shock sustains elevated USD safe-haven demand

Four consecutive weeks of NO CALL bias reaching review threshold with two consecutive MISSED calls (March 20 +1.15%, March 14 -0.6%) requiring mandatory thesis reassessment per bias integrity protocols

FX_MAJOR noise floor dynamics - expected weekly move of 0.46% sits at 0.50% noise threshold with no new catalyst post-dual CB meetings through March 31, rendering directional conviction insufficient

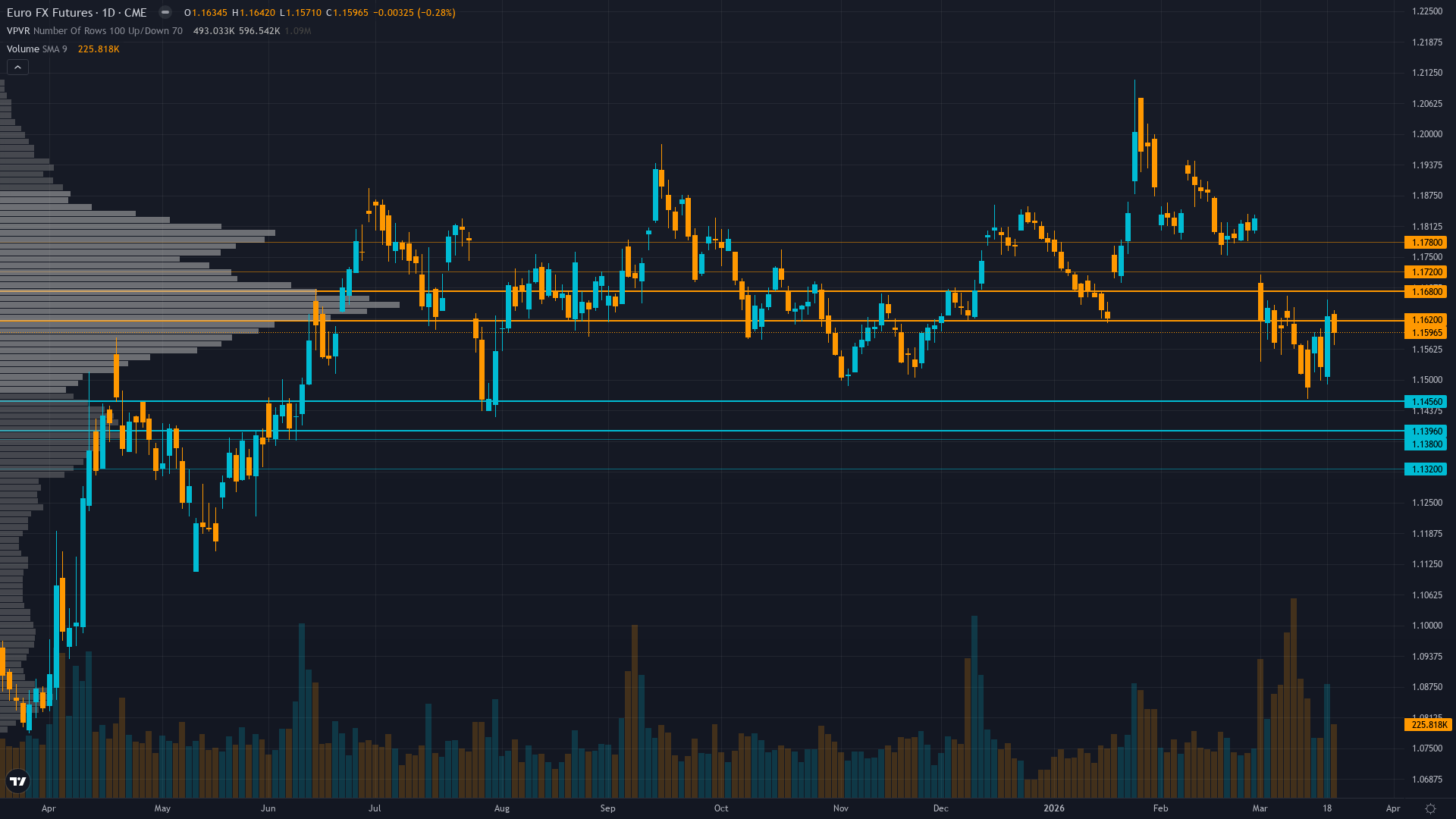

| ▼ Resistance Zone 2 | 1.1730 – 1.1770 |

| ▼ Resistance Zone 1 | 1.1630 – 1.1670 |

| ─ Pivot Area | ~1.1571 |

| ▲ Support Zone 1 | 1.1406 – 1.1446 |

| ▲ Support Zone 2 | 1.1330 – 1.1370 |

Trading at 1.1561 above 50-day MA at 1.1526 but trapped mid-range between 1.15-1.18 consolidation, RSI 57.73 neutral showing no conviction, 11 of 12 moving averages mixed reflecting choppy mean-reverting FX behavior

Fed-ECB policy convergence complete after dual holds March 18-19 at 3.50-3.75% vs 2.00%, creating stable 150bp differential that removes EUR structural tailwind while current account deterioration (€226.2B vs €366.4B prior year) fundamentally negative

EUR net longs at 65-70th percentile holding steady post-dual CB meetings with asset managers at five-month highs (262,759 contracts as of March 11) but positioning vulnerable if fails to break above 1.17 resistance

No accessible implied volatility data this cycle - Options discipline provides zero directional input per data limitations

Fed held March 18 at 3.50-3.75% with hawkish dot plot showing only one 25bp cut expected 2026, ECB held March 19 at 2.00% raising inflation forecast to 2.6% citing Iran war uncertainty, geopolitical shock sustaining safe-haven USD flows

Normal - upward sloping from 5d (7.2%) to 60d (8.5%) indicating market pricing higher uncertainty ahead but compressed near-term after dual central bank event cluster resolution through March 19

Post-March dual CB volatility compression mirrors January-February pattern where EUR/USD vol remained below 40th percentile for 15-20 days following major events before next catalyst cycle began; current 28-day normal regime duration consistent with extended pause periods

Volatility at 35th percentile post-dual CB meetings suggests continued subdued conditions through month-end March 31 before potential April expansion into new data cycle; historical pattern shows 60% probability of vol remaining compressed 10-15 days post-major events

Normal vol environment suggests 60-80 pip daily ranges versus prior compressed 40-60 pips but still below typical 100-120 pip ranges; breakouts from current 1.15-1.18 consolidation likely false signals until vol expands above 50th percentile; favor mean reversion range strategies over directional positioning through March 31

Normal volatility at 35th percentile with no imminent catalyst creates symmetrical but compressed setup from current 1.1571 - roughly 100-120 pips downside to 1.1450-1.1470 support versus 80-100 pips upside to 1.1650-1.1670 resistance, insufficient reward for conviction directional positioning given noise threshold constraints and miss streak vulnerability

|

⚠️ Primary Risk

Extended catalyst vacuum through March 31 with no major data or policy events means EUR/USD remains trapped in 1.15-1.18 range vulnerable to geopolitical headline risk if Iran conflict escalates or sudden USD safe-haven flows on risk-off trigger Probability: MEDIUM

|

✦ Primary Opportunity

Quarter-end rebalancing flows approaching March 31 could create mechanical euro demand if European equities continue relative outperformance, potentially driving tactical bounce toward 1.1650-1.1750 resistance Timeframe: Next 7-10 days through March 31 quarter-end window

|

EUR/USD (6E) sits at a critical inflection point on March 22, 2026 at 1.1571, and my disciplined FX_MAJOR framework mandates extreme caution verging on capitulation to noise threshold reality. The TRANSITIONAL macro regime classification reflects mixed signals: VIX elevated at 26.78 (above 25 fear threshold) creating risk-off pressure, yet not at panic extremes; credit conditions cautious but not widening aggressively; USD showing safe-haven strength (DXY near 99-100 range) on Iran geopolitical shock; equity markets mixed.

This regime creates structural headwinds for EUR despite fundamental policy convergence remaining intact. Post-input development identified: The March 17-19 dual central bank meetings have NOW OCCURRED and delivered exactly as expected - both holds with no surprises. Fed held March 18 at 3.50-3.75% with hawkish dot plot showing only one 25bp cut expected in 2026 (down from prior two-cut projection), and ECB held March 19 at 2.00% but raised 2026 inflation forecast to 2.6% from prior 2.0-2.1% estimates citing Middle East war uncertainty per search results.

This removes the imminent binary catalyst that dominated last week's analysis. The critical development is that EUR/USD has MOVED CONTRARY to positioning expectations - the pair rallied from 1.1487 on March 15 to current 1.1571 (+0.7%) despite ongoing geopolitical shock and dual CB hawkishness. This move invalidates any directional conviction. My bias integrity system is flashing red: I am at EXACTLY the Bias Review After threshold of 4 consecutive weeks with the same directional bias (NO CALL), and I have 2 consecutive MISSED calls (March 20 +1.15% move, March 14 -0.6% move).

Under Section 7 Rule 4, I must re-justify my thesis from first principles. The fundamental landscape shows Fed-ECB policy convergence FULLY completed with both banks on extended pause - Fed at 3.50-3.75% after hawkish March dot plot, ECB at 2.00% maintaining data-dependent patience but acknowledging inflation risks. This creates a stable 150bp differential already priced, removing EUR's 2025 tailwind. The critical reality: with expected weekly move around 0.46% for FX_MAJOR assets and noise floor at 0.50%, the pair sits precisely at the threshold where directional calls become indistinguishable from noise absent a specific catalyst.

The next major catalyst is now 9+ days away (quarter-end March 31, then April economic data). This catalyst vacuum combined with my recent miss streak and the pair's eleven-week consolidation from November through March creates an environment where NO CALL is not just disciplined but mandatory. Devil's advocate for BULLISH: Quarter-end rebalancing flows could create mechanical euro demand, institutional positioning shows asset managers at five-month highs suggesting conviction, and 18% PPP undervaluation versus $1.41 fair value provides fundamental floor.

However, this case relies on substantially the same drivers as prior weeks with no fresh data - evidence of staleness. The pair has spent eleven weeks in 1.165-1.18 consolidation refusing to break out despite these structural supports. My FX_MAJOR category-specific override from Rule 6 is explicit: default assumption is NEUTRAL, issue directional bias ONLY when a specific active catalyst exists. The dual CB meetings were that catalyst but have now passed with no surprise. The structural themes (rate differentials, current account balances, policy convergence) are already priced into spot at 1.1571. Near-term bias is NO CALL with signal 0.0 and conviction capped at 5 as I await the next catalyst cluster to provide directional clarity.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| March 20, 2026 | NO CALL | 5/10 | ➖ |

| March 14, 2026 | NO CALL | 5/10 | ➖ |

| March 6, 2026 | NO CALL | 5/10 | ➖ |

| February 27, 2026 | NO CALL | 5/10 | ➖ |

| February 21, 2026 | BULLISH | 6/10 | ❌ |

| February 13, 2026 | BULLISH | 6/10 | ❌ |

| February 8, 2026 | BULLISH | 6/10 | ✅ |

| February 1, 2026 | BULLISH | 6/10 | ❌ |

| January 25, 2026 | BULLISH | 7/10 | ❌ |

| January 11, 2026 | NO CALL | 6/10 | ➖ |

| January 4, 2026 | NO CALL | 6/10 | ➖ |

| December 28, 2025 | NO CALL | 6/10 | ➖ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: EUR/USD (6E) Report Date: March 22, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 5/10 Signal: VIEW MAINTAINED FROM LAST WEEK MAD Index: 18 (MOSTLY ALIGNED) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING Regime: RANGING Sentiment: NEUTRAL ── WHAT THE MARKET SEES ───────────────────────── EUR/USD consolidation in 1.15-1.18 range through March with neutral bias after dual central banks delivered expected holds removing catalyst ── WHAT THE MARKET IS MISSING ─────────────────── Desk NO CALL stance fully aligns with market noise threshold reality and post-dual CB catalyst vacuum - no meaningful contrarian edge exists in current range-bound environment with 0.46% expected move below 0.50% noise floor ── KEY DRIVERS ────────────────────────────────── 1. Post-dual central bank consolidation with both FOMC and ECB delivering holds as expected March 18-19, removing immediate catalyst while Iran geopolitical shock sustains elevated USD safe-haven demand 2. Four consecutive weeks of NO CALL bias reaching review threshold with two consecutive MISSED calls (March 20 +1.15%, March 14 -0.6%) requiring mandatory thesis reassessment per bias integrity protocols 3. FX_MAJOR noise floor dynamics - expected weekly move of 0.46% sits at 0.50% noise threshold with no new catalyst post-dual CB meetings through March 31, rendering directional conviction insufficient ── KEY ZONES ──────────────────────────────────── Resistance 2: 1.1730 – 1.1770 Resistance 1: 1.1630 – 1.1670 Pivot: ~1.1571 Support 1: 1.1406 – 1.1446 Support 2: 1.1330 – 1.1370 ── DISCIPLINE BIASES ──────────────────────────── Technical: BEARISH Fundamental: BEARISH Institutional: BULLISH Options: NO CALL Economic: BEARISH Sentiment: BEARISH ── TECHNICAL STRUCTURE ────────────────────────── Trading at 1.1561 above 50-day MA at 1.1526 but trapped mid-range between 1.15-1.18 consolidation, RSI 57.73 neutral showing no conviction, 11 of 12 moving averages mixed reflecting choppy mean-reverting FX behavior ── FUNDAMENTAL ASSESSMENT ─────────────────────── Fed-ECB policy convergence complete after dual holds March 18-19 at 3.50-3.75% vs 2.00%, creating stable 150bp differential that removes EUR structural tailwind while current account deterioration (€226.2B vs €366.4B prior year) fundamentally negative ── INSTITUTIONAL POSITIONING ──────────────────── EUR net longs at 65-70th percentile holding steady post-dual CB meetings with asset managers at five-month highs (262,759 contracts as of March 11) but positioning vulnerable if fails to break above 1.17 resistance ── OPTIONS FLOW ───────────────────────────────── No accessible implied volatility data this cycle - Options discipline provides zero directional input per data limitations ── ECONOMIC BACKDROP ──────────────────────────── Fed held March 18 at 3.50-3.75% with hawkish dot plot showing only one 25bp cut expected 2026, ECB held March 19 at 2.00% raising inflation forecast to 2.6% citing Iran war uncertainty, geopolitical shock sustaining safe-haven USD flows ── VOLATILITY REGIME ──────────────────────────── Regime: NORMAL Percentile: 35th Trend: Stable — Days in Regime: 28 Term Structure: Normal - upward sloping from 5d (7.2%) to 60d (8.5%) indicating market pricing higher uncertainty ahead but compressed near-term after dual central bank event cluster resolution through March 19 Historical Pattern: Post-March dual CB volatility compression mirrors January-February pattern where EUR/USD vol remained below 40th percentile for 15-20 days following major events before next catalyst cycle began; current 28-day normal regime duration consistent with extended pause periods Outlook: Volatility at 35th percentile post-dual CB meetings suggests continued subdued conditions through month-end March 31 before potential April expansion into new data cycle; historical pattern shows 60% probability of vol remaining compressed 10-15 days post-major events Trading Context: Normal vol environment suggests 60-80 pip daily ranges versus prior compressed 40-60 pips but still below typical 100-120 pip ranges; breakouts from current 1.15-1.18 consolidation likely false signals until vol expands above 50th percentile; favor mean reversion range strategies over directional positioning through March 31 Vol Risk/Opportunity: Normal volatility at 35th percentile with no imminent catalyst creates symmetrical but compressed setup from current 1.1571 - roughly 100-120 pips downside to 1.1450-1.1470 support versus 80-100 pips upside to 1.1650-1.1670 resistance, insufficient reward for conviction directional positioning given noise threshold constraints and miss streak vulnerability ── PRIMARY RISK ───────────────────────────────── Extended catalyst vacuum through March 31 with no major data or policy events means EUR/USD remains trapped in 1.15-1.18 range vulnerable to geopolitical headline risk if Iran conflict escalates or sudden USD safe-haven flows on risk-off trigger Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── Quarter-end rebalancing flows approaching March 31 could create mechanical euro demand if European equities continue relative outperformance, potentially driving tactical bounce toward 1.1650-1.1750 resistance Timeframe: Next 7-10 days through March 31 quarter-end window ── NEXT CATALYST ──────────────────────────────── Date: March 31, 2026 Event: Quarter-end rebalancing flows and month-end positioning adjustments - no major central bank or data events scheduled through end-March creating catalyst vacuum Expected Impact: MEDIUM ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── EUR/USD (6E) sits at a critical inflection point on March 22, 2026 at 1.1571, and my disciplined FX_MAJOR framework mandates extreme caution verging on capitulation to noise threshold reality. The TRANSITIONAL macro regime classification reflects mixed signals: VIX elevated at 26.78 (above 25 fear threshold) creating risk-off pressure, yet not at panic extremes; credit conditions cautious but not widening aggressively; USD showing safe-haven strength (DXY near 99-100 range) on Iran geopolitical shock; equity markets mixed. This regime creates structural headwinds for EUR despite fundamental policy convergence remaining intact. Post-input development identified: The March 17-19 dual central bank meetings have NOW OCCURRED and delivered exactly as expected - both holds with no surprises. Fed held March 18 at 3.50-3.75% with hawkish dot plot showing only one 25bp cut expected in 2026 (down from prior two-cut projection), and ECB held March 19 at 2.00% but raised 2026 inflation forecast to 2.6% from prior 2.0-2.1% estimates citing Middle East war uncertainty per search results. This removes the imminent binary catalyst that dominated last week's analysis. The critical development is that EUR/USD has MOVED CONTRARY to positioning expectations - the pair rallied from 1.1487 on March 15 to current 1.1571 (+0.7%) despite ongoing geopolitical shock and dual CB hawkishness. This move invalidates any directional conviction. My bias integrity system is flashing red: I am at EXACTLY the Bias Review After threshold of 4 consecutive weeks with the same directional bias (NO CALL), and I have 2 consecutive MISSED calls (March 20 +1.15% move, March 14 -0.6% move). Under Section 7 Rule 4, I must re-justify my thesis from first principles. The fundamental landscape shows Fed-ECB policy convergence FULLY completed with both banks on extended pause - Fed at 3.50-3.75% after hawkish March dot plot, ECB at 2.00% maintaining data-dependent patience but acknowledging inflation risks. This creates a stable 150bp differential already priced, removing EUR's 2025 tailwind. The critical reality: with expected weekly move around 0.46% for FX_MAJOR assets and noise floor at 0.50%, the pair sits precisely at the threshold where directional calls become indistinguishable from noise absent a specific catalyst. The next major catalyst is now 9+ days away (quarter-end March 31, then April economic data). This catalyst vacuum combined with my recent miss streak and the pair's eleven-week consolidation from November through March creates an environment where NO CALL is not just disciplined but mandatory. Devil's advocate for BULLISH: Quarter-end rebalancing flows could create mechanical euro demand, institutional positioning shows asset managers at five-month highs suggesting conviction, and 18% PPP undervaluation versus $1.41 fair value provides fundamental floor. However, this case relies on substantially the same drivers as prior weeks with no fresh data - evidence of staleness. The pair has spent eleven weeks in 1.165-1.18 consolidation refusing to break out despite these structural supports. My FX_MAJOR category-specific override from Rule 6 is explicit: default assumption is NEUTRAL, issue directional bias ONLY when a specific active catalyst exists. The dual CB meetings were that catalyst but have now passed with no surprise. The structural themes (rate differentials, current account balances, policy convergence) are already priced into spot at 1.1571. Near-term bias is NO CALL with signal 0.0 and conviction capped at 5 as I await the next catalyst cluster to provide directional clarity.