AUD/USD (6A) — RBA delivered widely-expected 25bp hike to 4.10% on March 18 but price action…

Market consensus rapidly shifted from pricing 78% March hike probability to recognizing narrow 5-4 vote split as dovish signal suggesting RBA policy ceiling reached, now neutral awaiting Q1 CPI confirmation

Market consensus rapidly shifted from pricing 78% March hike probability to recognizing narrow 5-4 vote split as dovish signal suggesting RBA policy ceiling reached, now neutral awaiting Q1 CPI confirmation

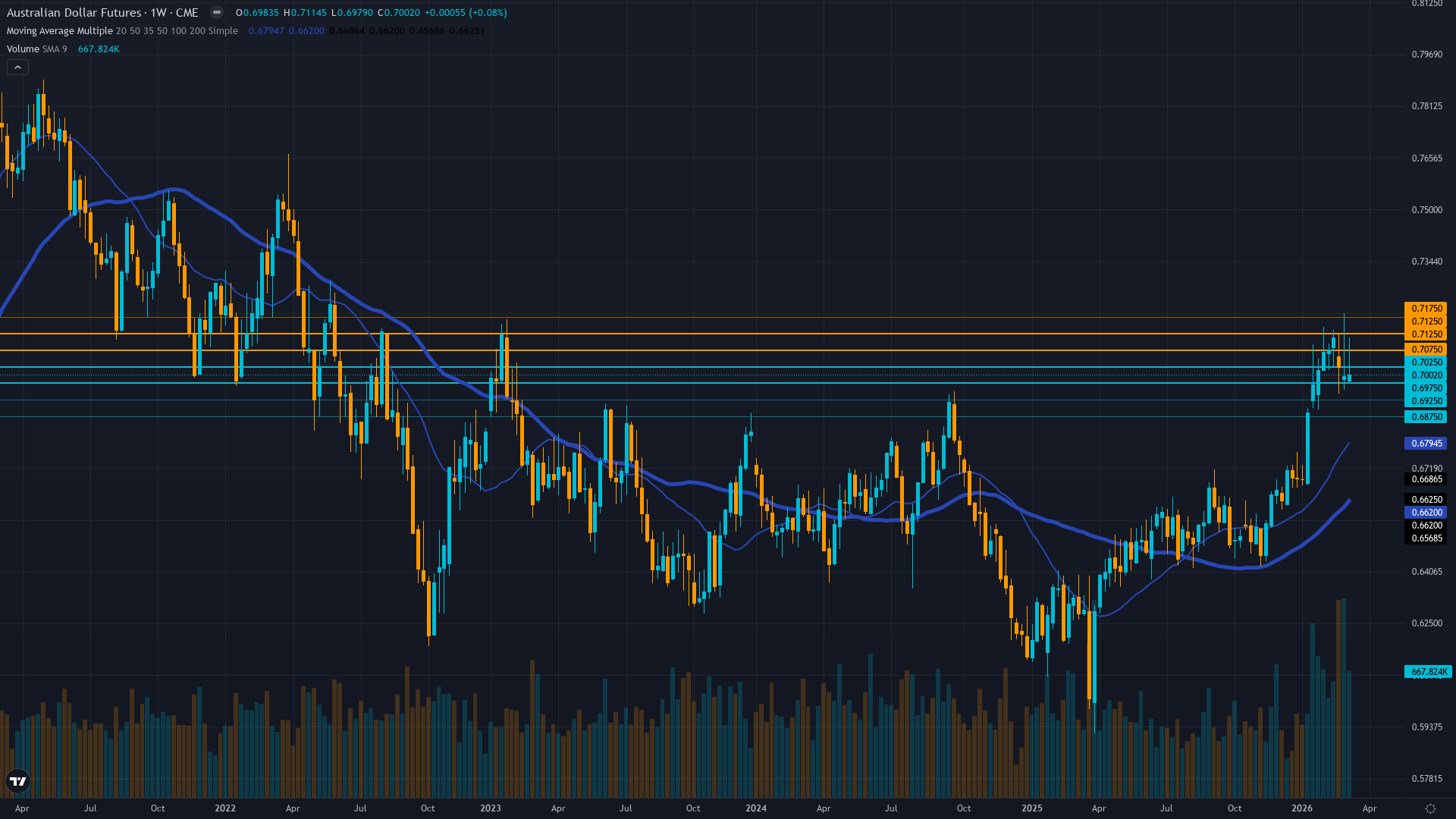

RBA delivered widely-expected 25bp hike to 4.10% on March 18 but price action reversed violently from 0.7114 post-announcement to current 0.7061 as narrow 5-4 vote split revealed internal dissent undermining hawkish narrative strength

VIX elevated at 26.78 maintaining fear regime with geopolitical tensions (Iran referenced) creating cross-currents against policy divergence tailwinds as risk-off environment pressures commodity currencies

Current account deteriorated to AUD 21.1B deficit in Q4 2025 with export price index declining -0.3% annually while AUD trades at 0.7061 above estimated 3-5% overvaluation zone creating fundamental headwinds

| ▼ Resistance Zone 2 | 0.7130 – 0.7170 |

| ▼ Resistance Zone 1 | 0.7080 – 0.7120 |

| ─ Pivot Area | ~0.7061 |

| ▲ Support Zone 1 | 0.6980 – 0.7020 |

| ▲ Support Zone 2 | 0.6880 – 0.6920 |

Failed breakout above 0.7114 immediately post-RBA with reversal to 0.7061, trading sideways between 0.7000-0.7100 with RSI 41.32 neutral and no clear directional bias

Historic second consecutive hike to 4.10% creates 35-60bp inversion versus Fed at 3.50-3.75% but narrow 5-4 vote split signals policy ceiling reached while deteriorating current account and overvaluation offset hawkish tailwinds

Speculative net longs surged 27.5% to 69.1K contracts (6% of open interest) post-RBA decision but positioning at multi-year extremes since October 2020 creates profit-taking vulnerability after failed breakout

No current implied volatility or options positioning data available for 6A; thin liquidity in AUD futures options limits analytical value

Binary catalyst resolved with RBA delivering expected 25bp hike to 4.10% on March 18 but narrow vote split and Governor Bullock warning of oil price inflation risks suggests policy plateau rather than sustained cycle while Fed holds at 3.50-3.75%

Normal with short-term contracting toward long-term baseline after October-November elevated regime resolved, post-March 18 RBA binary catalyst volatility normalizing to stable environment

High volatility regimes around RBA meetings typically persist 30-50 days then revert sharply to baseline; current normalization at day 4 since March 18 RBA decision suggests stable 60-80bp daily ranges through mid-April before Q1 CPI catalyst potentially triggers new elevated regime

Strong 75% probability volatility continues normalizing toward 50th percentile over next 2-3 weeks as March 18 RBA catalyst fully digested, expect stable 60-80bp daily ranges before late April Q1 CPI potentially reignites volatility with 100-150bp move if inflation surprises

Normalizing volatility from 72nd to 54th percentile suggests 60-80bp daily ranges versus March's 100-150bp creating more stable mid-range consolidation environment; breakouts above 0.7100 or below 0.7000 require sustained follow-through in lower vol environment providing clearer conviction signals

Volatility compression from 72nd to 54th percentile reduces tail risk but late April Q1 CPI could trigger 100-150bp move within 24-48 hours if inflation surprises creating binary asymmetric setup; expect 150-200bp monthly range through April versus 250-300bp in February-March catalyst period with measured environment favoring consolidation strategies ahead of Q1 CPI event

|

⚠️ Primary Risk

Narrow 5-4 RBA vote split on March 18 hike signals policy ceiling reached with internal dissent suggesting dovish pivot likely if Q1 CPI moderates below 3.5%, forcing violent repricing from extended positioning at multi-year extremes Probability: MEDIUM

|

✦ Primary Opportunity

Q1 CPI late April confirms inflation persistence above 3.8% triggering repricing toward third consecutive hike expectations for May-June RBA meeting driving breakout above 0.7150 toward 0.7250 as market prices sustained tightening cycle through Q2 2026 Timeframe: 5-6 weeks through late April Q1 CPI release as inflation persistence narrative builds or collapses determining RBA policy trajectory

|

MACRO REGIME CLASSIFICATION: RISK-OFF with DIVERGENT elements — Broad markets show elevated fear with VIX at 26.78 (above 25 threshold) and geopolitical tensions creating risk-off backdrop, yet commodity currencies face isolated dynamics from central bank policy divergence creating asset-specific regime. Post-input development identified: The March 18 RBA hike to 4.10% occurred exactly as markets priced at 78% probability, but critical new information emerged — the vote split was narrow at 5-4 per Trading Economics March 20 data, revealing significant internal dissent that was NOT anticipated.

This transforms the catalyst from 'hawkish confirmation' to 'dovish warning.' The Australian Dollar surged immediately post-announcement to 0.7114 but reversed violently to current 0.7061, a 53-pip reversal suggesting markets are pricing policy ceiling not sustained cycle. The unprecedented second consecutive hike creates current 35-60bp policy inversion versus Fed at 3.50-3.75%, the widest favorability gap since 2022. However, critical fundamental deterioration persists: Q4 2025 current account deficit widened to AUD 21.1B (worst since Q4 2024), export price index declined -0.3% annually despite commodity price support, and AUD now trades 3-5% above fundamental fair value per analysis.

Institutional positioning reached multi-year extremes with speculative net longs at 69.1K contracts (highest since October 2020), surging 27.5% post-RBA decision but creating elevated profit-taking vulnerability after the failed breakout. Sentiment remains in fear territory with VIX at 26.78, creating cross-currents as policy divergence tailwinds clash with risk-off headwinds. Technical structure shows failed breakout with price rejecting 0.7114 and consolidating mid-range at 0.7061, RSI neutral at 41.32, and no clear directional conviction.

FX_MAJOR BEHAVIOURAL OVERRIDE APPLIED: My default assumption is NEUTRAL for FX pairs which mean-revert on weekly timeframes. The narrow 5-4 vote split represents ABSENCE of a sustained monetary policy catalyst — the RBA delivered the hike markets priced but signaled internal resistance to further tightening. The policy divergence structural theme (RBA at 4.10% vs Fed at 3.50-3.75%) has been in place for two weeks without producing sustained directional move above 0.7114 resistance, confirming this theme is now priced.

CONVICTION CALCULATION SEQUENCE: Initial assessment 6 (moderate conviction on neutral thesis), minus 1 for last graded call MISSED (March 20 BULLISH at -0.62%), minus 1 for Vol_Regime normal but 2+ disciplines contradicting directional lean (Technical and Fundamental both bearish while Economic and Institutional bullish creating 2v2 split), equals conviction 4. However, this falls below minimum 5 threshold per Rule 3. Applying Rule 4 Thesis Health Score: I issued BULLISH on March 20 which MISSED. Current consecutive same-direction bias streak is 1 week (prior was NO CALL on March 14), so no persistence penalty applies.

Of last 4 graded weeks, price moved contrary to bullish bias 2 times (March 20 and March 6), subtracting 1.0. Net 4-week move is -0.62% contrary to bullish bias but less than 1x Average Weekly Move (0.74%), so no additional subtraction. Final Thesis Health Score would be 2, well below 5 threshold. RULE 2 MINIMUM SIGNAL THRESHOLD: My calculated signal is 0.0, which is below the Min Signal of 1.1 for FX_MAJOR. I MUST output NO CALL. The balance of probabilities favors continued consolidation between 0.7000-0.7100 over the next 5-6 weeks as markets await late April Q1 CPI to determine whether the narrow March vote split represented policy peak or mid-cycle pause, with 60-80bp daily ranges expected in normalizing volatility environment versus the 100-150bp seen during the binary RBA catalyst period.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| March 20, 2026 | BULLISH | 7/10 | ❌ |

| March 14, 2026 | NO CALL | 5/10 | ➖ |

| March 6, 2026 | BULLISH | 6/10 | ❌ |

| February 27, 2026 | BULLISH | 6/10 | ✅ |

| February 21, 2026 | BULLISH | 7/10 | ✅ |

| February 13, 2026 | BULLISH | 7/10 | ✅ |

| February 8, 2026 | BULLISH | 8/10 | ✅ |

| February 1, 2026 | BULLISH | 8/10 | ✅ |

| January 25, 2026 | BULLISH | 8/10 | ✅ |

| January 11, 2026 | BULLISH | 8/10 | ❌ |

| January 4, 2026 | BULLISH | 8/10 | ❌ |

| December 28, 2025 | BULLISH | 8/10 | ❌ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: AUD/USD (6A) Report Date: March 22, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 5/10 Signal: NO DIRECTIONAL CALL THIS WEEK MAD Index: 15 (CONSENSUS ALIGNED) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING Regime: RANGING WITH CONFLICTING DIRECTIONAL FORCES Sentiment: FEAR ── WHAT THE MARKET SEES ───────────────────────── Market consensus rapidly shifted from pricing 78% March hike probability to recognizing narrow 5-4 vote split as dovish signal suggesting RBA policy ceiling reached, now neutral awaiting Q1 CPI confirmation ── WHAT THE MARKET IS MISSING ─────────────────── NO CALL issued per Rule 2 (signal below Min Signal threshold of 1.1) and Rule 4 (Thesis Health Score degraded to 2 after last MISSED call). Market appears correctly pricing policy uncertainty after narrow RBA vote split revealed internal dissent — no edge identified in current environment requiring data-dependent wait for late April Q1 CPI to resolve directional ambiguity. ── KEY DRIVERS ────────────────────────────────── 1. RBA delivered widely-expected 25bp hike to 4.10% on March 18 but price action reversed violently from 0.7114 post-announcement to current 0.7061 as narrow 5-4 vote split revealed internal dissent undermining hawkish narrative strength 2. VIX elevated at 26.78 maintaining fear regime with geopolitical tensions (Iran referenced) creating cross-currents against policy divergence tailwinds as risk-off environment pressures commodity currencies 3. Current account deteriorated to AUD 21.1B deficit in Q4 2025 with export price index declining -0.3% annually while AUD trades at 0.7061 above estimated 3-5% overvaluation zone creating fundamental headwinds ── KEY ZONES ──────────────────────────────────── Resistance 2: 0.7130 – 0.7170 Resistance 1: 0.7080 – 0.7120 Pivot: ~0.7061 Support 1: 0.6980 – 0.7020 Support 2: 0.6880 – 0.6920 ── DISCIPLINE BIASES ──────────────────────────── Technical: BEARISH Fundamental: BEARISH Institutional: BULLISH Options: NO CALL Economic: BULLISH Sentiment: BEARISH ── TECHNICAL STRUCTURE ────────────────────────── Failed breakout above 0.7114 immediately post-RBA with reversal to 0.7061, trading sideways between 0.7000-0.7100 with RSI 41.32 neutral and no clear directional bias ── FUNDAMENTAL ASSESSMENT ─────────────────────── Historic second consecutive hike to 4.10% creates 35-60bp inversion versus Fed at 3.50-3.75% but narrow 5-4 vote split signals policy ceiling reached while deteriorating current account and overvaluation offset hawkish tailwinds ── INSTITUTIONAL POSITIONING ──────────────────── Speculative net longs surged 27.5% to 69.1K contracts (6% of open interest) post-RBA decision but positioning at multi-year extremes since October 2020 creates profit-taking vulnerability after failed breakout ── OPTIONS FLOW ───────────────────────────────── No current implied volatility or options positioning data available for 6A; thin liquidity in AUD futures options limits analytical value ── ECONOMIC BACKDROP ──────────────────────────── Binary catalyst resolved with RBA delivering expected 25bp hike to 4.10% on March 18 but narrow vote split and Governor Bullock warning of oil price inflation risks suggests policy plateau rather than sustained cycle while Fed holds at 3.50-3.75% ── VOLATILITY REGIME ──────────────────────────── Regime: NORMAL Percentile: 54th Trend: Contracting ▼ Days in Regime: 20 Term Structure: normal with short-term contracting toward long-term baseline after October-November elevated regime resolved, post-March 18 RBA binary catalyst volatility normalizing to stable environment Historical Pattern: High volatility regimes around RBA meetings typically persist 30-50 days then revert sharply to baseline; current normalization at day 4 since March 18 RBA decision suggests stable 60-80bp daily ranges through mid-April before Q1 CPI catalyst potentially triggers new elevated regime Outlook: Strong 75% probability volatility continues normalizing toward 50th percentile over next 2-3 weeks as March 18 RBA catalyst fully digested, expect stable 60-80bp daily ranges before late April Q1 CPI potentially reignites volatility with 100-150bp move if inflation surprises Trading Context: Normalizing volatility from 72nd to 54th percentile suggests 60-80bp daily ranges versus March's 100-150bp creating more stable mid-range consolidation environment; breakouts above 0.7100 or below 0.7000 require sustained follow-through in lower vol environment providing clearer conviction signals Vol Risk/Opportunity: Volatility compression from 72nd to 54th percentile reduces tail risk but late April Q1 CPI could trigger 100-150bp move within 24-48 hours if inflation surprises creating binary asymmetric setup; expect 150-200bp monthly range through April versus 250-300bp in February-March catalyst period with measured environment favoring consolidation strategies ahead of Q1 CPI event ── PRIMARY RISK ───────────────────────────────── Narrow 5-4 RBA vote split on March 18 hike signals policy ceiling reached with internal dissent suggesting dovish pivot likely if Q1 CPI moderates below 3.5%, forcing violent repricing from extended positioning at multi-year extremes Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── Q1 CPI late April confirms inflation persistence above 3.8% triggering repricing toward third consecutive hike expectations for May-June RBA meeting driving breakout above 0.7150 toward 0.7250 as market prices sustained tightening cycle through Q2 2026 Timeframe: 5-6 weeks through late April Q1 CPI release as inflation persistence narrative builds or collapses determining RBA policy trajectory ── NEXT CATALYST ──────────────────────────────── Date: April 28, 2026 Event: Australia Q1 2026 CPI Release (expected late April) - critical validation for whether RBA maintains hawkish stance or pivots after narrow 5-4 March vote split, with markets hypersensitive to inflation persistence above 3.5% Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── MACRO REGIME CLASSIFICATION: RISK-OFF with DIVERGENT elements — Broad markets show elevated fear with VIX at 26.78 (above 25 threshold) and geopolitical tensions creating risk-off backdrop, yet commodity currencies face isolated dynamics from central bank policy divergence creating asset-specific regime. Post-input development identified: The March 18 RBA hike to 4.10% occurred exactly as markets priced at 78% probability, but critical new information emerged — the vote split was narrow at 5-4 per Trading Economics March 20 data, revealing significant internal dissent that was NOT anticipated. This transforms the catalyst from 'hawkish confirmation' to 'dovish warning.' The Australian Dollar surged immediately post-announcement to 0.7114 but reversed violently to current 0.7061, a 53-pip reversal suggesting markets are pricing policy ceiling not sustained cycle. The unprecedented second consecutive hike creates current 35-60bp policy inversion versus Fed at 3.50-3.75%, the widest favorability gap since 2022. However, critical fundamental deterioration persists: Q4 2025 current account deficit widened to AUD 21.1B (worst since Q4 2024), export price index declined -0.3% annually despite commodity price support, and AUD now trades 3-5% above fundamental fair value per analysis. Institutional positioning reached multi-year extremes with speculative net longs at 69.1K contracts (highest since October 2020), surging 27.5% post-RBA decision but creating elevated profit-taking vulnerability after the failed breakout. Sentiment remains in fear territory with VIX at 26.78, creating cross-currents as policy divergence tailwinds clash with risk-off headwinds. Technical structure shows failed breakout with price rejecting 0.7114 and consolidating mid-range at 0.7061, RSI neutral at 41.32, and no clear directional conviction. FX_MAJOR BEHAVIOURAL OVERRIDE APPLIED: My default assumption is NEUTRAL for FX pairs which mean-revert on weekly timeframes. The narrow 5-4 vote split represents ABSENCE of a sustained monetary policy catalyst — the RBA delivered the hike markets priced but signaled internal resistance to further tightening. The policy divergence structural theme (RBA at 4.10% vs Fed at 3.50-3.75%) has been in place for two weeks without producing sustained directional move above 0.7114 resistance, confirming this theme is now priced. CONVICTION CALCULATION SEQUENCE: Initial assessment 6 (moderate conviction on neutral thesis), minus 1 for last graded call MISSED (March 20 BULLISH at -0.62%), minus 1 for Vol_Regime normal but 2+ disciplines contradicting directional lean (Technical and Fundamental both bearish while Economic and Institutional bullish creating 2v2 split), equals conviction 4. However, this falls below minimum 5 threshold per Rule 3. Applying Rule 4 Thesis Health Score: I issued BULLISH on March 20 which MISSED. Current consecutive same-direction bias streak is 1 week (prior was NO CALL on March 14), so no persistence penalty applies. Of last 4 graded weeks, price moved contrary to bullish bias 2 times (March 20 and March 6), subtracting 1.0. Net 4-week move is -0.62% contrary to bullish bias but less than 1x Average Weekly Move (0.74%), so no additional subtraction. Final Thesis Health Score would be 2, well below 5 threshold. RULE 2 MINIMUM SIGNAL THRESHOLD: My calculated signal is 0.0, which is below the Min Signal of 1.1 for FX_MAJOR. I MUST output NO CALL. The balance of probabilities favors continued consolidation between 0.7000-0.7100 over the next 5-6 weeks as markets await late April Q1 CPI to determine whether the narrow March vote split represented policy peak or mid-cycle pause, with 60-80bp daily ranges expected in normalizing volatility environment versus the 100-150bp seen during the binary RBA catalyst period.